If you prepare for remaining in your home for a long period of time-- Because you'll pay another collection of shutting costs with a reverse home loan, you require to remain in the home long enough to justify the cost. So, if you're 62, have a background of durability and also think your current location is your permanently home, a reverse home loan could make good sense. Plus, if you reside in a market where house values are appreciating at a fast clip, your residential or commercial property may deserve plenty extra by the time you or your successors repay http://codysgfa988.yousher.com/5-kinds-of-mortgage the finance. A vital part of examining whether a reverse mortgage is ideal for you or otherwise is figuring out why you truly need the funds.

- If you did spend the cash, you would certainly owe it and also would certainly start to build up passion owed on the money you did spend for as lengthy as it continued to be impressive on the line.

- HECMs were developed in 1988 to assist older Americans make ends meet by permitting them to use the equity of their residences without needing to leave.

- The unfavorable equity defenses enacted in 2012 forbid both of those circumstances.

- Key distinctions in between reverse home mortgages in Canada versus the united state

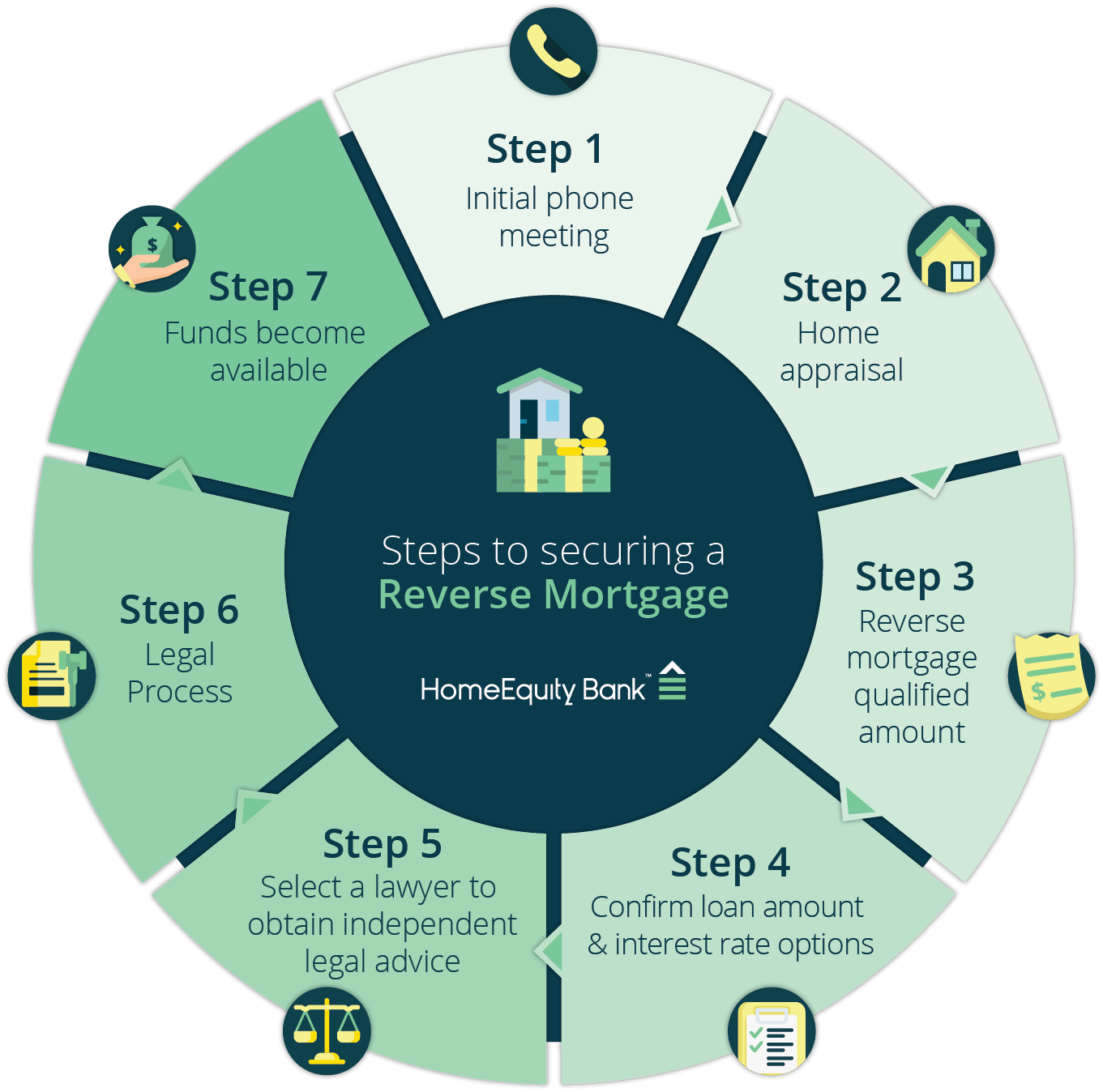

- Reverse home mortgages absolutely fulfill a requirement in the marketplace, however they are not fit for all senior citizens.

When you move out, you still get the SPIA repayments. Reverse mortgages can use up the equity in your house, which suggests less properties for you and your successors. The majority of reverse mortgages have something called a "non-recourse" provision. This suggests that you, or your estate, can't owe greater than the value of your house when the car loan becomes due and also the home is sold. With a HECM, normally, if you or your successors intend to pay off the finance and also maintain the residence instead of market it, you would certainly not need to pay greater than the evaluated value of the residence. Every lender is various and charges a different set of costs.

This is why there are hardly ever CHIP Reverse Home mortgage issues for heirs; after the house is marketed as well as the home loan settled, there is generally a large amount of money left over. Another 90-day expansion can be requested, once more with HUD's authorization. If your accumulated passion as well as principal get to the value of your home, you won't get kicked out as a result of a forced sale, nor have financial debt proceed building up. The negative equity defenses enforced laws in 2012 forbid both of those situations.

Various Other Insurance Coverage

Your proportion of equity decreases in time, to cover the costs you pay. As we've seen above, a number of the regarded CHIP Reverse Home loan troubles are just not true. Nonetheless, one vital reality regarding reverse home mortgages is that they offer protection for many Canadians during their retired life, as well as minimized financial tension and also a much better quality of life. This is just one of one of the most typical reverse home loan myths and also is definitely false. You are not required to make any type of regular monthly repayments in any way, so you can't miss any.

Your successors will certainly never need to pay more than the complete car loan equilibrium or 95 percent of the home's appraised worth, whichever is much less. If you have a Home Equity Conversion Home mortgage your successors will have to pay off either the complete financing equilibrium or 95% of the home's assessed worth-- whichever is less. MyBankTracker produces income via our relationships with our companions as well as affiliates. We may point out or consist of testimonials of their products, at times, yet it does not influence our referrals, which are completely based on the research study and job of our content team. We are not contractually obligated by any means to supply favorable or recommendatory evaluations of their solutions. Currently, there is just one jumbo reverse home loan loan provider in the nation-- somebody who will certainly make you a car loan for greater than $625,500.

I Have A Line Of Credit, When Can My Lender Start To Bill Interest On The Funds?

Nonetheless, if you remain in a vendor's market you'll likely need to pay a costs for your brand-new, smaller space. However, retaining your home equity without taking out a reverse mortgage can be a much more appealing-- as well as less expensive-- way to cover costs in retirement. While a reverse mortgage may seem like a great way to access money in your golden years, it's important to recognize the truths of this kind of loan. [newline] Below's how you can anticipate to take advantage of a reverse home loan-- and what to watch out for when contrasting this finance choice to other options. One of the most considerable risk with a reverse home loan is that the interest charges substance and try your equity.

Maintain Your Heirs Notified

You remain to reside in your house and retain the title to it. Similar to any kind of home mortgage, you must fulfill your funding responsibilities, maintain existing with real estate tax, insurance policy, upkeep, and also any kind of house owners association costs. The reverse mortgage has come to be an important financial choice for numerous Canadian retired people. Reverse home mortgages are expanding by over 28% every year and also it's understandable Click for more info why. Retirees are increasingly residence abundant as well as cash inadequate.

Reverse home mortgages often are marketed to retirement-age homeowners who want more money to Visit the website cover living costs however still intend to hold on to their residences. Among the upsides of a reverse home loan is that lending institutions typically do not enforce earnings or credit history demands. A reverse mortgage makes it possible for home owners, especially those who are of old age, to obtain versus the equity in their residences. One advantage of a reverse home loan is that lenders don't usually have minimal revenue or credit history demands, which can help house owners looking to cover living expenses. A residence equity lending is a bank loan that's secured by the consumer's house equity and also paid in a round figure. Similarly, a home equity line of credit-- or HELOC-- lets property owners borrow versus their equity approximately a specific limitation and accessibility those funds on an as-needed basis.

Please seek advice from a legal representative, monetary consultant or real estate counselor prior to you make any type of decisions. Customers that choose a fixed price finance will get a single disbursement round figure settlement. Various other financing settlement choices are readily available just for adjustable price mortgages.